THE ROLE OF CASH FLOWS IN THE FINANCIAL MANAGEMENT OF THE ENTITY

1. Introduction – Cash Flows

Most of the time, cash flows are used for determining the liquidity lacks of an entity. When used as a financial instrument (for example for determining the internal profitability rate), it is recommended to structure cash flow on different types of flows. Another reason for this determination is the fact that cash flow reports are easier to interpret under this form, in comparison to the profit and loss account.

From the structure of this financial reporting, there results that there are several cash input and output flows included in the total sum of cash flows:

Flows from the operational activity: cash receivable or payable during the unfolding of the main business. This measures the cash generated or used by the company as a result of goods or services production or sale. Even if under certain circumstances there is expected that these operational flows should be negative (for example in the case of rapid economic growths), for most companies, positive flows are essential for the long term survival. The funds generated from the operational activity may be used for paying dividends, credits and replacing the production capacity or investing in new acquisitions.

The cash flows from the investment activity is represented by the cash receivable or payable for buying or selling equipment or other fixed assets required for maintaining the operational capacity and for insuring the future development of the enterprise.

The cash flows from the financing activity are formed by the cash receivable or payable during the movements between the company, some debtors and creditors. This flow includes earnings from issuing bonds, payment for dividends, reimbursement of loans etc.

This financial report presenting cash inflows and outflows during a period of time is called cash-flows report.

During this period of time, cash flow presents the way in which the changes produced in the balance sheet and in the profit and loss account influences the earnings of the entity and groups them in three categories of activities: operational, financial and investment.

Cash-flow report is at the same time an analytical financial instrument for determining the short term viability of the company, especially its capacity of paying debts. In international accounting, cash flow reports are regulated by IAS 7.

Cash flow reports are very important for the newly founded companies with limited liquid assets. These companies are vulnerable to liquidity crisis even when the receivables account from the checking balance sheet show, on a long term period, a healthy financial standing.

In the profit and loss account, the profit reported is not cashed in the moment of its reporting, due to the engagement accounting. On the other hand, the expenses reflected in the profit and loss account are only partially paid for. If the balance sheet presents from a static point of view the financial standing of the entity, the cash flow report or treasury flow statement is a dynamic statement, integrating information from the balance sheet and from the profit and loss account. That is why, in practice, this financial instrument can be successfully used, as we will further present.

The cash – flow from operational activities is compared to the net profit of the company. If the cash flow from operational activity is higher then the net profit it is said that the net profit of the company is “of high quality”. If the cash flow from operational activity if lower then the net profit, there should be a reason why the net profit does not change into cash.

2. The analysis of cash flows based on an indicators system

The analysis of a company’s treasury flows is not complete unless we highlight a system of indicators that should contribute to the dynamics of the financial management of the entity.

In order to evaluate liquidity, the informational system of the entity enables the utilization of the following indicators:

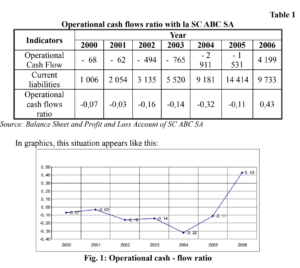

a. Operational cash flow ratio, determined by the model:

Operational cash flow ratio = Operational cash flow/Current liabilities (1)

The indicator measures the liquidity of the entity by comparing the actual cash flow (in stead of current and potential cash resources) with current liabilities. This ratio evaluates the way in which current liabilities are covered by the cash – flow generated from the activity of the company. Through this calculation method it is avoided the transformation of current assets into cash.

With SC ABC SA the situation in dynamics of this indicator is presented as follows:

The data of the table and the graphic above show the fact that SC ABC SRL has high debts, which cannot be easily covered from the operational cash flow. This means that the entity analyzed had to use external financing in order to ensure the required liquidities for continuing its current activity, excepting the last year analyzed, when the cash generated by the operational activity covered 43% of the current liabilities of the company.

b) Another indicator showing the reconciliation between profit and the treasury of the enterprise, due to engagement accounting, is represented by the net profit ratio calculated as percent between net profit and cash flow from operational activity.

Net profit ratio = Net profit/Operational cash – flow (2)

The indicator shows the contribution of net profit to the generation of cash flows from operational activity.

In the case of the analyzed enterprise, there is noticed that, during the entire analyzed period, the net profit plays a major role in generating cash flows from operational activity, but the variation of the working capital consumed the cash surplus represented by the net profit.

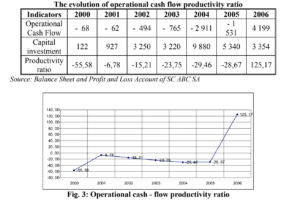

c) The contribution of the operational activity to the partial or total financing of productive investments may be highlighted with the help of operational flows productivity ratio calculated as percent between the cash flow from the operational activity and the entity’s investments in fixed assets.

The productivity ratio of operational cash flow = Operational Cash flow/ Total asset acquisitions (3)

From the data presented above, there results that, excepting 2006; the exploitation activity did not ensure the required funds for financing the investment activities of SC ABC SA.

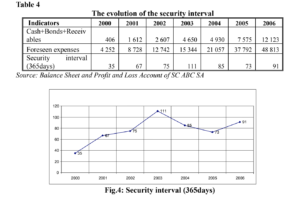

d) An indicator evaluating the dependence of the company’s liquidities of its activity is “the security interval”.

The security interval, in contrast to the other indicators presented above, ensures an intuitive evaluation of the company’s liquidity, even if it is a more restrictive one. This indicator compares immediate cash sources (cash, bonds, receivables) to the estimated cash outputs required for the normal unfolding of the company’s activity: foreseen expenses. There are different definitions of cash resources and foreseen expenses. A basic formula would be the following:

Security interval = 365 x Cash + Bonds + Receivables/Foreseen expenses (4)

With SC ABC SA, seen in its evolution, the situation of this indicator is presented below (table 4 and figure 4):

From the data presented in the table and graphic above there results that, during the entire analyzed period of time, SC ABC SA ensured the financing of the activity from cash resources or future cashing. Thus, in 2000, financing is ensured for 35 days; in 2001, financing is ensured for 67 days; in 2002, financing is ensured for 75 days, in 2003, financing is ensured for 111 days, in 2004, financing is ensured for 85 days, in 2005, financing is ensured for 73 days and, in 2006, financing is ensured for 91 days.

From what we presented above there results that each component of the total cash flow bases on the two “pillars”: cashing and payment. That is why the expanding of the analysis has to be made on these two components of the treasury, referring in fact to the administration of the enterprise’s monetary resources.

3. Conclusions

Some investors believe that “cash is king”. The cash flow report identifies the cash entering and exiting the company. If a company constantly generates more cash then it uses, it will be able to increase dividends, purchase stocks, reduce debts or buy another company.

Certain financial models are based on the cash flow report. A report of The Research Institute Council called “The Future Shape of Financial Reports” recommended a series of reforms [Arnold John, 1991]. One of the most important possibilities of improving has been the reporting on the position of the company’s cash. Professor John Arnold says: “little attention is to be paid to the reporting on the company’s cash or the liquidity position. Cash represents the blood of each business of the entity”[Arnold John, 1991].

An important issue is the relation that can be established between cash flows and profit and loss account, since cash flows do not represent an alternative for the profit and loss account.

The financial viability and the future survival of any organization consist of the capacity of generating a positive cash flow. Cash flow helps reducing the dependence of the organization on external funds, the fulfillment of the duty service and liabilities, the accomplishment of financial investments and the offering the investors an acceptable dividend policy. The final result is that, irrespective of the profit reported, if the organization is not able to generate enough cash, it will go bankrupt.

Cash flow statement may be also used for evaluating any economic decision and shows the economic performance of the organization. The decisions made on the basis of cash flow expectancies can be followed and revised any time additional information on cash are available.

The quality of the information contained in “Cash flow statement” is better then the information contained in “Funds flow statement”, since it is more consistent and neutral. Cash flows may be more credible followed when there is a transaction going on, while funds flows are distorted by inherent accounting judgments [Crichton John,1990].

Any information on the dimension, synchronizations and security of the future cash of the company on cashing and payment are useful in evaluating solvability.

The best method for evaluating the success of a business is when the enterprise generates cash inflows higher then outflows. The essence of a business management is of attracting resources and of using them so that there should be obtained product for which people would pay more then their original cost. In our opinion, no enterpriser can maintain in a business unless it obtains from it more money then he/she invested. That is why; the first financial function that an enterprise has to assume is treasury administration that is ensuring solvability with minimum financial and administrative expenses.

It is important to that the notion of cash flow should be separated by the notion of accounting result, since only in this way there can be explained why an enterprise that made profit can meet difficulties in paying its current liabilities. Managers should understand that an accounting loss does not necessarily mean a cash loss” and that the successes or failures of the enterprise should not be analyzed starting only with the accounting results, since liquidity and profit are completely different, but complementary indicators and characterize the financial standing of the company.

Cash flow and treasury do not mean by themselves the financial performance of the enterprise’s activity. The best evidence in this sense is that the enterprise may obtain positive treasury flows even if it recorded accounting losses, or it may record negative treasury flows even if it made profit.

We cannot equalize cash flow and the profit obtained from the activity of an enterprise, reason why also the opinions of the specialists are divided.

We believe that cash flow should represent for any manager a permanent science for adopting a financial strategy that should keep the business going.

REFERENCES

1. Arnold John and others (1991) – The Future Shape of Financial Reports, ICAEW an ICAS;

2. Arnold John (1991) – The Future Shope of Financial Reports, Accountancy, May;

3. Crichton John (1990) – Cash-flow Statements – What are the choice?, Accountancy, October.

Coautor: Dr. Larissa BĂTRÂNCEA Babes-Bolyai University Cluj-Napoca